All Categories

Featured

Table of Contents

When life stops, the dispossessed have no selection but to keep moving. Almost right away, family members should take care of the difficult logistics of death complying with the loss of a loved one. This can include paying bills, dividing possessions, and managing the funeral or cremation. Yet while fatality, like tax obligations, is inescapable, it does not have to problem those left.

In addition, a full fatality advantage is often offered for unexpected death. A modified fatality benefit returns costs typically at 10% passion if fatality takes place in the first 2 years and involves the most kicked back underwriting.

To finance this business, companies count on personal health and wellness interviews or third-party information such as prescription histories, fraud checks, or motor lorry documents. Underwriting tele-interviews and prescription histories can typically be made use of to assist the representative finish the application process. Historically companies depend on telephone interviews to confirm or validate disclosure, but more lately to boost consumer experience, business are depending on the third-party information suggested over and giving immediate decisions at the factor of sale without the meeting.

Assured For Life Funeral Plan

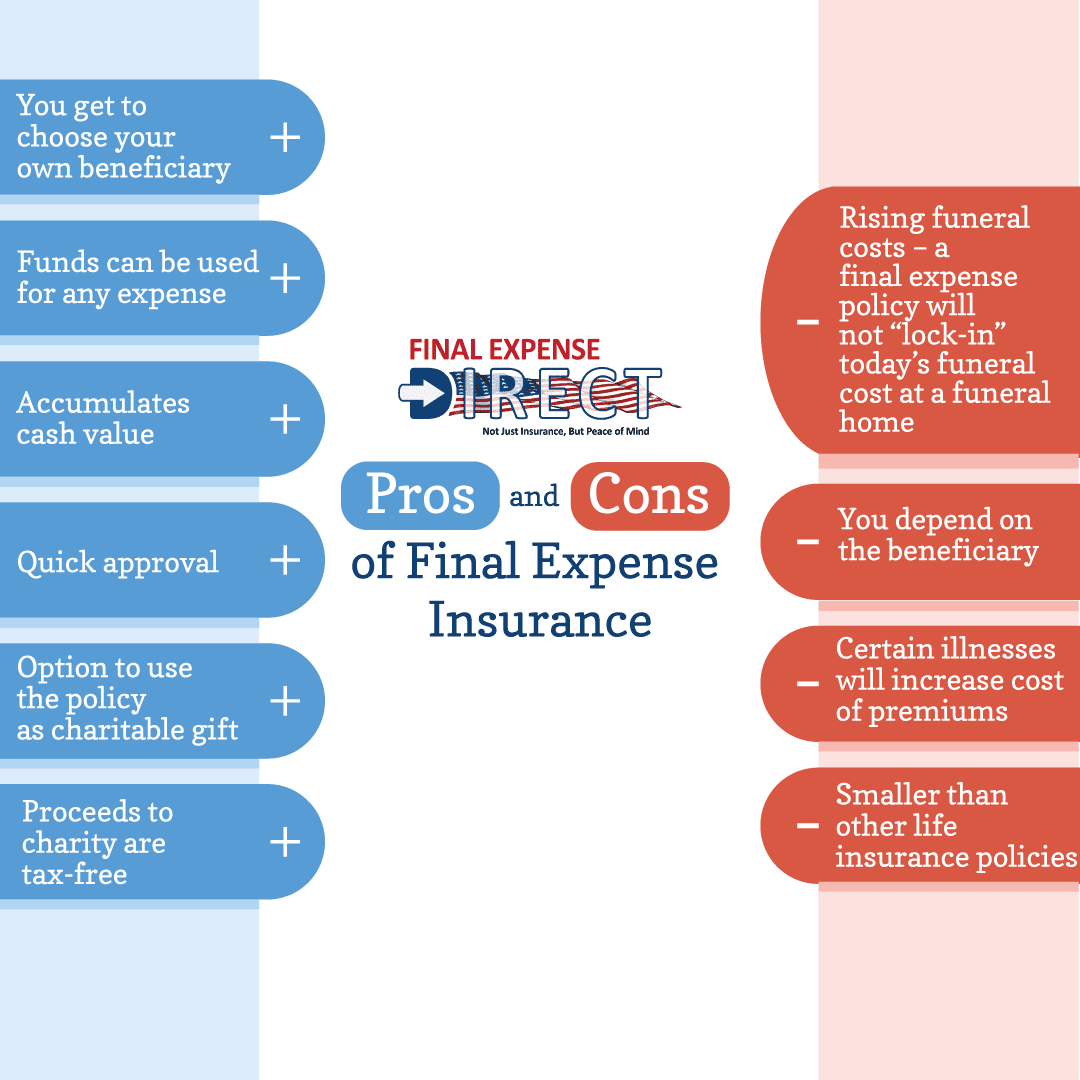

But what is last expenditure insurance, and is it constantly the finest path forward? Listed below, we have a look at exactly how final expenditure insurance works and elements to think about before you purchase it. Technically, last expense insurance is a entire life insurance policy plan specifically marketed to cover the expenditures related to a funeral, memorial solution, function, cremation and/or interment.

While it is explained as a plan to cover last expenditures, beneficiaries who receive the death advantage are not required to use it to pay for final costs they can use it for any kind of function they like. That's due to the fact that final cost insurance truly falls under the group of modified whole life insurance policy or streamlined concern life insurance policy, which are generally whole life policies with smaller sized survivor benefit, usually between $2,000 and $20,000.

Our opinions are our own. Funeral insurance is a life insurance plan that covers end-of-life expenses.

Difference Between Burial Insurance And Life Insurance

Interment insurance requires no clinical test, making it available to those with clinical problems. This is where having funeral insurance, also understood as last cost insurance coverage, comes in useful.

Streamlined concern life insurance coverage calls for a health and wellness evaluation. If your health and wellness status invalidates you from conventional life insurance policy, burial insurance coverage may be an option.

Compare budget-friendly life insurance policy alternatives with Policygenius. Besides term and irreversible life insurance, interment insurance policy is available in numerous kinds. Take a look at your protection options for funeral service expenditures. Guaranteed-issue life insurance policy has no health needs and offers fast approval for insurance coverage, which can be helpful if you have extreme, incurable, or numerous health problems.

Cheap Burial Insurance

Simplified issue life insurance does not call for a medical examination, yet it does call for a health questionnaire. This policy is best for those with light to modest wellness conditions, like high blood pressure, diabetic issues, or asthma. If you don't want a medical exam yet can get approved for a simplified problem plan, it is normally a better deal than an assured problem plan because you can get more insurance coverage for a cheaper costs.

Pre-need insurance policy is high-risk due to the fact that the beneficiary is the funeral home and coverage specifies to the chosen funeral chapel. Must the funeral home go out of service or you relocate out of state, you might not have insurance coverage, which defeats the purpose of pre-planning. In addition, according to the AARP, the Funeral Consumers Alliance (FCA) discourages purchasing pre-need.

Those are basically funeral insurance coverage plans. For guaranteed life insurance, premium calculations depend on your age, sex, where you live, and protection quantity.

Burial insurance uses a streamlined application for end-of-life protection. Most insurance coverage business require you to speak with an insurance policy agent to use for a policy and obtain a quote. The insurance agents will request for your individual details, get in touch with information, financial details, and insurance coverage preferences. If you decide to purchase an assured concern life policy, you will not need to undertake a medical examination or questionnaire.

The objective of living insurance coverage is to ease the problem on your liked ones after your loss. If you have an extra funeral service policy, your liked ones can make use of the funeral plan to take care of final expenses and get a prompt dispensation from your life insurance policy to deal with the home loan and education prices.

Individuals who are middle-aged or older with clinical conditions might consider interment insurance coverage, as they might not get traditional policies with stricter authorization criteria. In addition, interment insurance can be valuable to those without considerable savings or conventional life insurance coverage. Burial insurance policy differs from various other kinds of insurance policy because it provides a lower fatality benefit, usually just adequate to cover expenses for a funeral service and other associated prices.

Life Insurance For Cremation

News & World Record. ExperienceAlani has examined life insurance policy and pet dog insurer and has written many explainers on traveling insurance, credit scores, financial debt, and home insurance coverage. She is passionate regarding debunking the intricacies of insurance and various other personal finance topics to ensure that viewers have the information they require to make the very best money choices.

The more protection you obtain, the greater your costs will certainly be. Last expense life insurance has a number of advantages. Namely, everyone who uses can get accepted, which is not the instance with various other kinds of life insurance policy. Last expense insurance is often recommended for elders who may not get typical life insurance coverage as a result of their age.

On top of that, final expense insurance policy is helpful for people that wish to pay for their very own funeral. Interment and cremation solutions can be costly, so final expense insurance policy offers tranquility of mind recognizing that your liked ones will not have to utilize their financial savings to pay for your end-of-life arrangements. Final cost insurance coverage is not the ideal product for everybody.

The Best Funeral Plan

Getting whole life insurance policy with Principles is fast and very easy. Coverage is readily available for elders between the ages of 66-85, and there's no clinical examination needed.

Based upon your reactions, you'll see your approximated rate and the quantity of protection you get (in between $1,000-$30,000). You can purchase a policy online, and your insurance coverage starts quickly after paying the first premium. Your price never ever alters, and you are covered for your whole lifetime, if you proceed making the monthly repayments.

Ultimately, we all need to think of exactly how we'll pay for a liked one's, or even our very own, end-of-life expenditures. When you market final cost insurance coverage, you can provide your customers with the assurance that includes understanding they and their family members are prepared for the future. You can also obtain an opportunity to maximize your book of business and produce a new income stream! Prepared to discover whatever you need to recognize to begin marketing last expense insurance policy efficiently? No one likes to think concerning their very own fatality, but the reality of the issue is funeral services and funerals aren't low-cost.

In enhancement, clients for this kind of plan could have serious legal or criminal backgrounds. It is very important to note that various carriers use an array of concern ages on their guaranteed concern plans as low as age 40 or as high as age 80. Some will certainly additionally use greater face worths, as much as $40,000, and others will certainly enable for better fatality advantage problems by improving the rates of interest with the return of costs or reducing the number of years till a full survivor benefit is readily available.

{kind=link}

Latest Posts

Benefits Of Burial Insurance

Funeral Expenses Insurance Policy

Difference Between Burial And Life Insurance